London's stock market has plunged following the UK's referendum vote to leave the EU.

The FTSE 100 index began the day by falling more than 8%, then regained some ground to stand nearly 5% lower.

Banks were hard hit, with Barclays and RBS falling about 30%, although they later pared losses to below 20%.

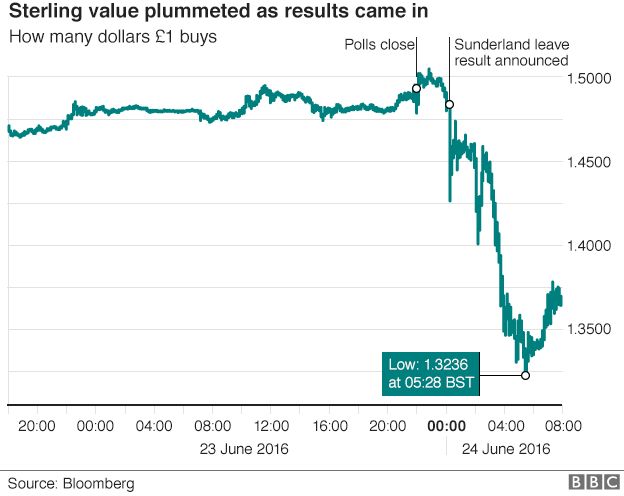

Earlier, the pound fell dramatically as the referendum outcome emerged. At one stage, it hit $1.3236, a fall of more than 10% and a low not seen since 1985.

By lunchtime, it had partially recovered, but was still nearly 8% down on the day.

The

Bank of England said it was "monitoring developments closely" and would

take "all necessary steps" to support monetary stability.

"This is simply unprecedented, the pound has fallen off a cliff and

the FTSE is now following suit," said Dennis de Jong, managing director

of UFX.com.

"Britain's EU referendum has been a cloud hanging over

the global economy for the past few months and that cloud has got very

dark this morning.

"The markets despise uncertainty, yet that is

exactly what they're faced with this morning. The shockwaves are likely

to reverberate for some time and the warning lights are flashing

brighter now than ever."

The FTSE's initial slump was its biggest one-day fall since the collapse of Lehman Brothers in October 2008.

As well as the banks, the housebuilding sector was also badly hit, with shares in Bovis Homes down more than 20% by lunchtime.

UK

government bond yields hit a new record low, with 10-year yields down

more than 30 basis points to 1.018%, according to Reuters data.

Two-year yields fell more than 20 basis points to their lowest levels since mid-2013, at 0.233%.

The

impact of the vote was also felt in other European countries. The Paris

and Frankfurt indexes were both down more than 7%, while the Swiss

central bank intervened on the money markets to steady the Swiss franc

after it appreciated in value.

Oil prices have also fallen sharply in the wake of the referendum outcome, with Brent crude down 5.2%.

The

price of Brent crude fell by $2.63 to $48.28 a barrel, its biggest fall

since February. At the same time, US crude was down 5.1%, or $2.54, to

$47.57 a barrel.

'Once-in-a-lifetime moves'

Before the results started to come in, the pound had risen as high as $1.50, as traders bet on a Remain victory.

But following early strong Leave votes in north-east England, it

tumbled to $1.43 and then took another dive after 03:00 BST as Leave

maintained its lead.

The move in sterling is the biggest one-day fall ever seen.

A

weaker pound buys fewer dollars or other foreign currencies, which

makes it more expensive to buy products from abroad. However, it should

benefit exporters as it makes their goods cheaper abroad.

Against the euro, the pound dropped 7% to about €1.2085. By Friday lunchtime, it had risen again but was still 5.3% down on the day.

At one point, the euro was 3.3% lower against the dollar, its biggest one-day fall since the currency's inception.

Currency traders say these moves are more extreme than those seen during the financial crisis of 2008.

"Leave's victory has delivered one of the biggest market shocks of all time," said Joe Rundle, head of trading at ETX Capital.

"The pound has collapsed to its lowest level in over 30 years, suffering its biggest one-day fall in living memory.

"Panic

may not be too strong a word - the pound could have further to go over

the next couple of days as markets digest the news.

"It's fair to

say we've never seen anything like it and the chances are markets will

remain highly volatile over the coming hours and days."

IAG, which owns British Airways and Iberia, issued a statement saying the result of the vote would hit its profits.

"Following

the outcome of the referendum, and given current market volatility,

while IAG continues to expect a significant increase in operating profit

this year, it no longer expects to generate an absolute operating

profit increase similar to 2015," it said.

'Contingency plans'

'Contingency plans'

David

Tinsley at UBS said there would be "a significant rise in economic

uncertainty" and that the Bank of England's Monetary Policy Committee

(MPC) was expected to take action, including interest rate cuts and an

extension of its quantitative easing programme.

"We expect the MPC

will cut policy rates to zero and make further asset purchases, in the

first instance of £50-75bn, not later than February 2017," he said.

In

a statement, Bank of England governor Mark Carney said the Bank would

"pursue relentlessly" its responsibilities for monetary and financial

stability, which were unchanged.

He said the Bank had put in place

"extensive contingency plans" to mitigate the risks associated with the

referendum, adding that it stood ready to provide more than £250bn of

additional funds to banks through its normal facilities.

"In the coming weeks, the Bank will assess economic conditions and will consider any additional policy responses," he said.

The

European Central Bank (ECB) also issued a statement saying it was

closely monitoring financial markets and was in close contact with other

central banks.

"The ECB stands ready to provide additional liquidity, if needed, in euro and foreign currencies," it added.

No comments:

Post a Comment